News Release

Private-Sector Retirement Plans Play Increasingly Important Role Across All Incomes

Study Examines Evolution of Retirement Income Since 1974 ERISA

Washington, DC, November 18, 2010 - Across all income groups, retirement income from employer-sponsored retirement plans is more prevalent among retirees today than in the mid-1970s, when sweeping new retirement plan regulations were enacted, according to a new study released by the Investment Company Institute.

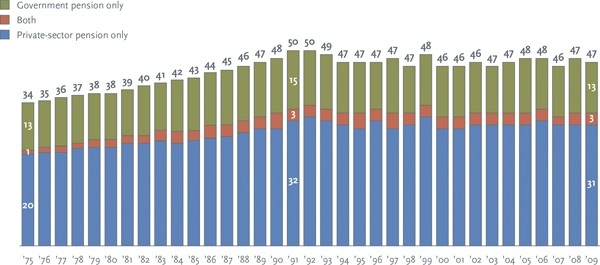

The study, A Look at Private-Sector Retirement Plan Income After ERISA, finds that in 2009, 34 percent of retirees received income—either directly or through a spouse—from private-sector retirement plans, compared with 21 percent in 1975. The median income received by those with private-sector pension income increased to $6,000 in 2009 from about $4,500 in 1975 (in 2009 dollars). The research examines private-sector retirement income trends since 1975 just after the Employee Retirement Income Security Act (ERISA) was enacted.

Receipt of Income from Pension by Type of Pension

(Percentage of retirees* with type of pension, 1975–2009)

*Individuals aged 65 and older with non-zero income and not working; for married couples, neither the individual nor the spouse worked. Sample excludes highest 1 percent and lowest 1 percent of the income distribution.

Source: ICI tabulations of the March Current Population Survey

“Looking at the entire period from 1975 to 2009, the data show that, contrary to conventional wisdom, private-sector pension income has become more prevalent, not less prevalent, over time,” said Peter Brady, ICI senior economist and co-author of the report. “Retirement policy discussions often seem to start from the premise that retirees’ pension income has fallen over time. This report refutes that belief and provides some historical context for these policy discussions by examining trends in retiree income from private-sector pensions.”

Evolution of Employer-Sponsored Retirement Plans Since ERISA

U.S. worker access to private-sector retirement plans has remained pretty consistent since the 1970s. While coverage has been consistent, an increasing share of private-sector workers has worked for employers that sponsor defined contribution (DC) pension plans, and a decreasing share has worked for employers that sponsor defined benefit (DB) pension plans. In 1975, 87 percent of active participants in private-sector retirement plans had primary coverage through DB plans, dropping steadily over time to below 50 percent by the 1990s. By 1998, 56 percent of active participants in private-sector retirement plans were covered by a primary DC plan, and 39 percent had a supplemental DC plan.

“Coverage” Does Not Always Result in Pension Income

The historical prevalence of retirement income from private-sector DB plans may be overstated by only looking at pension coverage, rather than receipt of pension income. Many employees may have worked for companies that offered DB plans, but, because private-sector workers change jobs often, the combination of vesting rules and back-loaded benefit accrual resulted in many retirees getting little or no retirement income from the plans.

“There seems to be a belief that there was a golden age of pensions—a time in our history when most private-sector workers retired with a monthly pension check that replaced a significant amount of their salary. The facts support a different narrative: there was no golden age,” said Brady. “The good news is private-sector retirement income has increased over time and, to date, the shift from DB pensions to DC pensions has not led to a decline in private-sector pension income. Furthermore, the typical amount of private-sector pension income that we observe in the historical data can be generated by relatively modest accumulations in DC plans or IRAs.”

Ongoing Role of Social Security in Retirement

Since 1975, there has been little change in the importance of Social Security benefits in providing retiree income: Social Security benefits continue to serve as the foundation for retirement security in the U.S. and represent the largest component of retiree income and the predominant income source for lower-income retirees. In 2009, Social Security benefits were 58 percent of total retiree income and more than 85 percent of income for retirees in the lowest 40 percent of the income distribution. Even for retirees in the highest income quintile, Social Security benefits represented more than one-third of income in 2009.